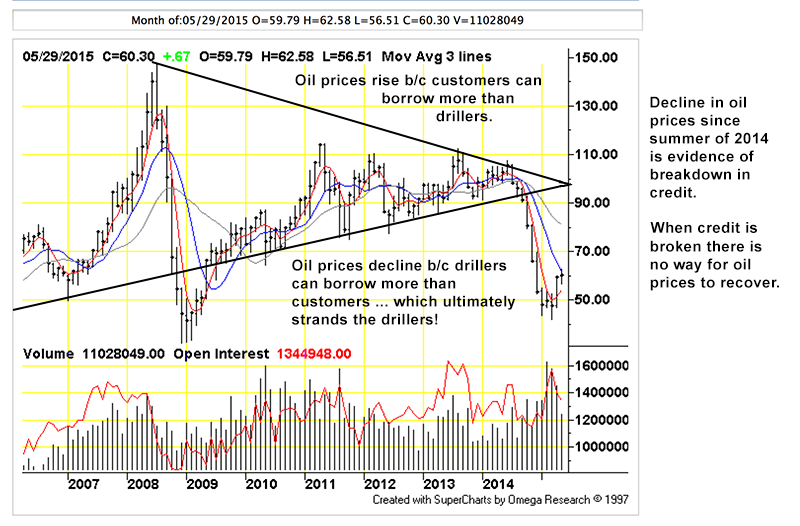

Figure 1: Triangle of you-know-what, continuous WTI futures contracts, chart by TFC Charts, (click for big). Petroleum price decline is just one piece of evidence for credit distress; another is the steady increase in bond yields which reflects the anxiety on the part of lenders that they might not be repaid.

It is difficult to make heads-or-tails out of the Greek melodrama playing out at this moment. To default or not default, in the eurozone or out. Who knows? Observers are confused and so are the participants, what is clear is that the stakes are very high. The group designated to absorb the hardest blows cling to the bottom of the economic mast; workers, pensioners, students and suckers lured into investing in countries like Greece … then again, maybe not. There is the chance of contagion, anything is possible including the chance that some tycoons might lose their fortunes.

Regardless of outcome, the politicians are winners. Even as their follies multiply they meet nothing in the way of discomfort. Walking on gilded splinters, they spend every moment within settings as extravagant as Hollywood sets, fawned over by hordes of lackeys. Stuffed like geese for foix-gras on mysterious ‘luxury food’, their greatest hazard is that they might get too fat … or that they might be revealed as libertines. When their crimes and blunders have ripened they retire with their fortunes; enormous (borrowed) pensions, favorable (borrowed) business arrangements, excessive (borrowed) speaking fees and … (borrowed) … consulting jobs even as their constituents are hounded into penury so as to make the interest payments.

Other winners include the ordinary ‘Brand X’ criminals who take advantage of the vacuum that is the natural outcome of their betters’ ineptitude. Misery multiplies … none of this is new. The die for the current round of crises was cast long before the turn of the millennium … there has been that long to do something about it.

One thing is clear; that the brouhaha in credit markets is a symptom, not the disease. Analysts must observe carefully the larger trends and connect the dots. The problem is not a matter of adjusting the model but with the model itself. Industrial enterprise does not offer a return. Capital and value — and purchasing power — are converted into waste, what stands for ‘wealth’ is a measurement of the wasting process. Our economy has bloated into a monstrous organism that consumes everything and puts nothing back. The disease is the reaching of planetary limits; access to water, fuel, minerals, soil fertility, waste-carrying capacity and credit. Capital resources are being allocated by rationing access to loans. No credit = no resources, taking place under everyone’s nose is ‘Conservation by Other MeansTM‘.

This is a nasty and unpredictable process, what connects the dots together is the common outcome: ‘less’.

The one fact about parties is that they all end. The cocaine runs out. Everyone has to go home.

In the Eurozone and elsewhere, the cocaine — cheap credit — is running out. What remains is the hangover and daunting task of sobriety. Along with the credit, going is the gasoline. Things will never be the same.

‘Never be the same’ are fighting words for the Establishment which entrenches itself more deeply into the present even as both it and establishment become less relevant. Because it has lost the ability to reform itself, the establishment lashes out in a reflexive attempt to preserve its vanishing prerogatives. This is self-evident: if reform was possible it would have already taken place, the reforms would have prevented the crises.

Managers do not grasp the currency risk that emerges from both continued austerity programs or default. Economies are containers of social- and political values, shared understanding built upon edifices of trust. Within economies a collective suspension of disbelief takes place that insists bits of colored paper or electronic data are worth something. The trust emerges as more people share the same ‘worth’ idea and gain benefits from it.

Germany is Europe’s responsible party, it is EU’s paymaster and the long-time primary beneficiary of the Euro-economic activity. Mercantile Germany sits at the center of Continental trade; German euro surpluses are the consequence of its partners’ deficits. Ironically, German currency risk is no different from Greek risk, because both countries do business in what amounts to a foreign currency. Germany holds a borrowing advantage at the moment but both are built with the same financial armature, the defects of one country are the defects of all the others. The idea that Germany can integrate Europe around its economy … then somehow pull up the ladder when convenient is a hallucination.

Presently, managers carelessly discount one group’s sense of worth then another’s. Today is Greece, tomorrow is another country. Trust wavers then evaporates, at that point the economy is junk and the money is worthless, even if ‘the numbers’ indicate otherwise.

Reckless Germany gambles with euro risk even as it cannot afford to do so. It holds trillions of EU liabilities both in the form of currency and credits in its banking system along with ongoing business relationships with companies outside of Germany and the Eurozone. German wealth is nothing other than the trust earned over the entire post-WWII period. The ideal is that each European will engage profitably with others; not as slaves, some paying while others collect. Germany pretends it controls its destiny but this is something it cannot guarantee. Trust cannot be directly inserted into the minds of others: what Germany has cultivated carefully with one hand it casually undermines with the other.

Right now Germany plays the part of enforcer for Europe’s criminal banks. The blows it levels against its neighbors rebound against itself; the outcome of this is slow suicide. The impaired assets on European balance sheets outweigh investor equity and bondholder credit together. Europe is insolvent, liabilities are looking for a place to hide. The logical destination is Germany whether there is a euro or not. Within the euro, Germany cannot escape the full weight of its neighbors’ liabilities. Consequently, it has no choice but to succeed at its unification endeavor … otherwise, the worthlessness of the others’ balance sheets will be marked up against its own.

German banks and industry are right now stuffed with euros but this is momentary. There is no way possible for the current conditions within German finance to survive the demise of the currency. Germany cannot simply pick up its luggage and move itself away from Europe taking its ‘wealth’ with it. There is no road map for Germany to get from the euro to a substitute currency space The Germans and other creditor countries frozen to the spot: any sign that the Germans might abandon the euro would be the alarm for the others to do the same, to the instant ruin of German creditors, who are owed tens of trillions of euros.

The end of the euro anywhere within the Eurozone would also cast into doubt the security of Germany’s bank deposits. Uncertainty would trigger a run on German banks just as there is a run on Greek banks today. Germany would find itself bound by domestic politics to defend the euro to the bitter end, to protect its depositors. By doing so, Germany would become the fool of the market, the dumping ground for all European liabilities. This is a fate it cannot avoid, because of its long-running success it is the only European country with money!

The alternative strategy would have Germany racing Greece and Italy out the door. The survivor would be the first to grab a lifeboat on the Titanic. This is the nature of unraveling Ponzi schemes where the few winners get out early.

Add the currency trap to Keynes’ liquidity trap amplified by the political expediency trap. In its desire to party forever Europe is confronted with the persistence of liabilities that are generated along the way. These liabilities pitch Germany’s tent on the lip of the abyss. With the passage of time and accumulating mis-management, holders question whether euros are ‘worth the hassle’ and ‘worth the risk’ or not. This is not the proper sort of inner dialog to have about any currency.

With a non-euro currency, Germany’s option would be to depreciate. Doing so at a scale that would ‘manage’ liabilities would be default by another name with the costs falling on German depositors. To choose otherwise and not depreciate would leave Germany facing the same ruin as Greece faces right now; it would ‘become’ Greece, with massive and unsupportable demands for repayments in a foreign currency, a shortage of money, the absence of liquidity and a breakdown of export trade.

The only way for Germany to manage EU-legacy repayment claims would be to re-denominate them from euro to d-mark and then somehow inflate them away against a background of economic growth. However, jettisoning the euro would cut Germany off from its now-captive European markets. This would eliminate the growth potential; Germany would be crushed by its debts in a deflationary environment.

As bad as conditions would be for Germany, they would be worse for the other European countries. There would be a scramble for hard currency: everyone for themselves. If this is to be a hard German currency there would be a shortage much worse than there is today. The Europeans would be faced with the task of cobbling together a monetary system while the rubble of the current regime collapses on its head. Constructing a new model would require enormous investment of funds and good will that the Continent does not now possess; a breakdown would remove any possibility of either, there would be insufficient capital with which to (re)build anything.

The euro monetary union has had obvious structural defects from the get-go as admitted to by the Euromasters themselves. Now there is resolute refusal to address these defects even as the entire European enterprise accelerates to destruction. If not now, when? Does Angela Merkel or Wolfgang Schäuble honestly believe the Greeks will ever trust the Germans again after such rough treatment at the hands of faceless Troika functionaries? What good can this portend for German business? How do German businessmen expect their enterprises to succeed, on what alternative planet?

Dire times are when political instincts abandon professional politicians at a moment when these instincts are necessary. The Germans refuse to share any of the hardships their policies inflict upon their neighbors. Germans whine but their finance industry underwrote the bad loans, with eyes wide open, for the benefit of German manufacturers … whose ‘goods’ cannibalize the trading partners’ capital. German finance ignored the risks as it ignores currency risk today.

There are depositors run from Greek- and other banks into Northern Europe. The run itself is a part of the long-standing flow of funds from the rest of Europe into Germany’s national account. The ‘First Law’ states that as surpluses increase, the cost of managing them becomes greater than the surpluses’ worth. This can be seen in Europe where cost of Germany’s current account surplus is a shortage of liquidity and broken markets. Germany must unwind its surpluses, reducing the costs to both its customers and itself. It can unwind its smug sense of institutional superiority at the same time.

Europe has been in a finance crisis for years, there has been plenty of time to ‘innovate’ solutions. Sadly for the Euros, all of the real solutions require giving up something … which nobody wants to do. Instead there is punishment for those tied to the mast; the workers, pensioners, students and suckers lured into investing in countries like Greece. The best the bosses have come up with so far is bailouts for giant banks, ‘appropriation’ of depositor funds and (incoherent) public relations.

Europe needs debt relief and stringent energy conservation. Finance collapse turns out to be the implement of conservation as bankrupt Europeans cannot drive, small countries with nothing to offer but their own worthless currencies cannot import fuel. Finance dares not risk relief to Greece because it cannot withstand the losses. Relief to Greece means granting relief to other Euro-deadbeats France and Italy (Germany). What is taking place right now is a margin call against the euro. The absence of relief insures the collapse of the entire finance edifice as defaults proliferate and distrust propagates.

In Part II we will look at some of the steps that can be taken including The Greek government issuing non-liability fiat euros — Greenbacks — and use them to retire euro denominated obligations on a fixed schedule.