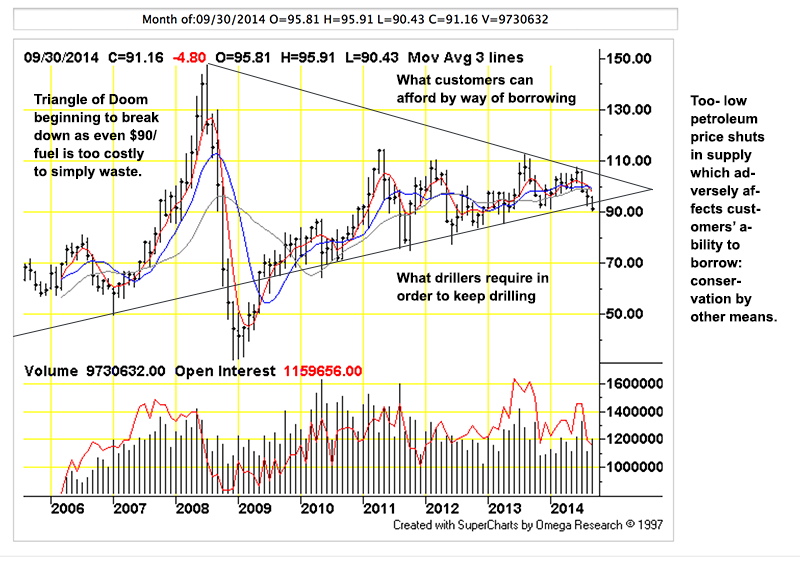

Figure 1: classic doomsday scenario as fuel prices begin to decline below what drillers require to bring new fuels to the marketplace. Fuel shortages do not drive prices higher; instead, capital depletion is reflected by the parallel decline of purchasing power. Customers are unable to gain credit while banking/finance systems break down. (Chart by TFC Charts, click on for big.)

Every part of the world is experiencing distress as modernity requires cheap fuel and other resources to squander. Since 2000, waste- for- pleasure confronts resources increasingly priced in line with their value; resources that are becoming too costly to waste. Sadly, we humans never figured out alternative uses for our capital, the time to find such uses has run out.

Sumitomo’s US shale oil foray turns sourBen McLannahan

Sumitomo Corp of Japan has drawn a line under its disastrous two-year foray into shale oil in the US, with writedowns connected to the project almost completely erasing its full-year earnings.

On Monday, Sumitomo, the fourth biggest of Japan’s trading companies by market capitalization, said that an impairment loss of Y170bn ($1.6bn) on a “tight oil” project in west Texas would form the bulk of Y240bn of charges for the fiscal year to March 2015.

… on Monday, Sumitomo said it had decided to sell roughly three-quarters of its acreage, triggering the loss on the assets and the agreement to fund their development. “It is difficult to extract the oil and gas efficiently,” the company said, adding that it could not “expect as much production to recover the investment”.

Other Japanese trading companies have taken big writedowns as shale bets have soured. Itochu Corp, the third largest trader by market capitalization, has written down about four-fifths of the Y78bn it paid in 2011 for a 25 per cent stake in family-owned Samson Investment of the US.

More Failure, Tim Morgan (Telegraph UK):

Shale has been hyped (“Saudi America”) and investors have poured hundreds of billions of dollars into the shale sector. If you invest this much, you get a lot of wells, even though shale wells cost about twice as much as ordinary ones.If a huge number of wells come on stream in a short time, you get a lot of initial production. This is exactly what has happened in the US.

The key word here, though, is “initial”. The big snag with shale wells is that output falls away very quickly indeed after production begins. Compared with “normal” oil and gas wells, where output typically decreases by 7pc-10pc annually, rates of decline for shale wells are dramatically worse. It is by no means unusual for production from each well to fall by 60pc or more in the first 12 months of operations alone.

Faced with such rates of decline, the only way to keep production rates up (and to keep investors on side) is to drill yet more wells. This puts operators on a “drilling treadmill” (running with the Red Queen), which should worry local residents just as much as investors. Net cash flow from US shale has been negative year after year, and some of the industry’s biggest names have already walked away.

The seemingly inevitable outcome for the US shale industry is that, once investors wise up, and once the drilling sweet spots have been used, production will slump, probably peaking in 2017-18 and falling precipitously after that. The US is already littered with wells that have been abandoned, often without the site being cleaned up.

2017-18 is optimistic. Drilling is undermined by an overall shortage of credit; oil prices are declining b/c oil customers around the world are bankrupt. Declining wages and the inability to ‘earn’ by wasting petroleum means customers cannot borrow, they are insolvent.

Loans are made to firms, instead; they are larger, they can offer up their leases as collateral. The result is that customers are starved for funds. Credit turns out to be another non-renewable resource; drillers compete against their own customers — and their lenders as well — to gain access to loans.

Energy Commodity Futures

| Commodity | Units | Price | Change | % Change | Contract |

|---|---|---|---|---|---|

| Crude Oil (WTI) | USD/bbl. | 87.67 | -1.18 | -1.33% | Nov 14 |

| Crude Oil (Brent) | USD/bbl. | 91.60 | -0.51 | -0.55% | Nov 14 |

| RBOB Gasoline | USd/gal. | 232.05 | -4.78 | -2.02% | Nov 14 |

| NYMEX Natural Gas | USD/MMBtu | 3.86 | -0.10 | -2.40% | Nov 14 |

| NYMEX Heating Oil | USd/gal. | 258.23 | -2.50 | -0.96% | Nov 14 |

Precious and Industrial Metals

| Commodity | Units | Price | Change | % Change | Contract |

|---|---|---|---|---|---|

| COMEX Gold | USD/t oz. | 1,221.20 | +8.80 | +0.73% | Dec 14 |

| Gold Spot | USD/t oz. | 1,220.56 | -0.58 | -0.05% | N/A |

| COMEX Silver | USD/t oz. | 17.38 | +0.14 | +0.81% | Dec 14 |

| COMEX Copper | USd/lb. | 302.75 | -1.15 | -0.38% | Dec 14 |

| Platinum Spot | USD/t oz. | 1,279.31 | -0.44 | -0.03% | N/A |

Table by Bloomberg, A decline in prices from current levels will reveal the fracking enterprise as a Ponzi scheme. This will in turn upset markets which have been promoting fracking returns as a ‘sure thing’, both for finance as well as for the consumption economy as a whole. Meanwhile, energy company internals deteriorate further, (Bloomberg):

Drillers Piling Up More Debt Than Oil Hunting Fortunes in ShaleAsjylyn Loder

Floyd Wilson raps his fingertips against the polished conference table. He’s just been asked, for a second time, how he reacted when his Halcon Resources Corp. (HK) wrote off $1.2 billion last year after disappointing results in two key prospects.

Wilson once told investors that the acreage might contain the equivalent of 1.2 billion barrels of oil. He fixes his interlocutor with a blue-eyed stare and leans forward. At 67, he bench-presses 250 pounds (110 kilograms) and looks it. Outside the expansive windows of his 67th-floor executive suite, downtown Houston steams in its July smog.

He responds, unsmiling, with a one-syllable obscenity: “F—.”

Wilson has reason to curse, Bloomberg Markets magazine will report in its October issue. On the wall behind him hang framed stock certificates of the four public energy companies he’s built in his 44-year career. The third, Petrohawk Energy Corp., discovered the Eagle Ford shale, now the second-most-prolific oil formation in the country. He sold Petrohawk three years ago for $15.1 billion.

Then came Halcon. Since Wilson took over as chairman and chief executive officer in February 2012, the company’s shares have dropped by about half, trading at $5.67 on Sept. 5.

Halcon spent $3.40 for every dollar it earned from operations in the 12 months through June 30. That’s more than all but six of the 60 U.S.-listed companies in the Bloomberg Intelligence North America Independent E&P Valuation Peers index. The company lost $1.4 billion in those 12 months. Halcon’s debt was almost $3.2 billion as of Sept. 5, or $23 for every barrel of proved reserves, more than any of its competitors.

Figure 2: the first appearance of the Triangle of Doom, in October, 2012. Economists fail to predict crashes and other events, their models are not particularly useful. At the same time, non-economists have little difficulty predicting onrushing adversity: in 2007, almost everyone in the real estate industry was concerned about questionable loan origination and underwriting. Most economists ignored the warning signs, just like they do today.

Zero-percent interest rates, direct asset purchases and swaps by central banks, stock market rigging and propaganda have had the affect of pushing oil driller credit costs as low as possible, resulting in a modest increase in the flow of unconventional petroleum. This increase has been sufficient to offset declines in conventional plays elsewhere in the world but not enough to support our ‘affluence lifestyles’ built around waste. This leaves us with the choice to conserve voluntarily or for conservation to be forced upon us by events.